Verona, 8/6/2025

Consolidated Financial Results as at 30th June 2025

REVO: STRONG GROWTH AND ONGOING VALUE CREATION

Half-year premiums reached €200.5 million (+31.0%), with a sharp increase in adjusted operating profit(1) €25.8 million (+54%), supported by resilient capital solidity and a combined ratio(2) of 83.2%.

- Gross written premiums € 200.5 million

- Insurance revenues € 135.2 million

- Adjusted operating profit € 25.8 million

- Net profit € 11.3 million

- Adjusted net profit € 15.0 million

- Group Solvency II ratio(3) 245.2%

Verona, 7 August 2025 – The Board of Directors of REVO Insurance S.p.A., parent company of the REVO Insurance Group, approved today the Consolidated Financial Results as of 30 June 2025.

KEY INDICATORS

- Gross written premiums of €200.5 million, up +31.0% compared to the same period in 2024 (€153.1 million).

- Growth in any business line, further diversifying the business mix.

- Adjusted operating profit of €25.8 million, showing a strong increase compared to the same period in 2024 (+53.8%), confirming the operational growth trajectory outlined in the Industrial Plan.

- Strong technical profitability, with a loss ratio(4) of 32.3%, higher than in H1 2024 (29.4%) but fully in line with medium-term targets and consistent with business development and diversification.

- Positive investment contribution of €3.8 million (€2.4 million in 2024) maintaining short duration and broad geographical diversification of the assets held in the portfolio.

- IT investment plan (approx. €5 million during the half-year) and operating cost trends in line with Plan trajectories.

- Consolidated net profit of €11.3 million (€15.0 million adjusted), up from €9.4 million and €11.2 million respectively in the same period of 2024.

- Solid capital position confirmed, with a Group Solvency II ratio at 245.2%.

Alberto Minali, Chief Executive Officer of REVO, stated: “By the end of the first half of 2025, we had already achieved two-thirds of the adjusted operating result of the entire year 2024. Our path of profitable growth confirms the strength of our trajectory and the consistency of the strategic choices outlined in the new Industrial Plan. This result reflects the effectiveness of a distinctive business model that positions technology as the engine of our development and leverages the relationship with intermediaries as a strategic driver for penetrating the SME and professionals’ market.”

STRATEGIC PERFORMANCE

During the half-year, REVO continued to advance the implementation of its 2026–2028 Industrial Plan, presented to the market June 2025:

- Significant growth of the broker channel, which generated approximately 53% of total GWP, marking a +38% increase compared to the same period in 2024. At the same time, partnerships managed through REVO Underwriting were further strengthened, with an increase of +33 relationships compared to the first half of 2024 and a +57% rise in premium volumes.

- Enlargement of the insurance solutions offered to our clients, with the launch of two new business lines: Credit and Energy, designed to provide tailored solutions to key industrial sectors within Italy’s productive ecosystem.

- Further expansion of the parametric offering accompanied by the introduction of instant payment features, which have reduced settlement times. The Protezione Consumi policy and the partnership with Spiagge.it have maintained a steady growth rate. In the travel sector, REVO has also signed a partnership with ADR Mobility for the launch of Volo Protetto, further strengthening its leadership in the travel market that demands accessible, fast, and transparent protections. In the first half of the year, the number of issued parametric policies amounted to approximately 44,000, compared to about 10,000 in the first half of 2024.

- Continued enhancement of the AI partner ecosystem—Liquidate, Luminate, and Operate— integrated within VERO platform. The new features improve efficiency in claims handling, communication automation, and back-office processes, enabling increasingly smart, fast, and accurate operational management.3

- Ongoing recruitment efforts, with 32 new hires, primarily in the Underwriting and Data & Artificial Intelligence areas.

- Approximately €4.5 million in premiums underwritten by REVO Iberia in the first half, supported by the expansion of commercial relationships—now totalling 42 local and international brokers—and the strengthening of the team with four new hires. The new Head of Claims - a key role to complete the operational structure - will join us in September.

- S&P rating confirmed at A- with a stable outlook, and Standard Ethics ESG rating confirmed at “EE” (equivalent to “strong” on the Standard Ethics scale), with a positive outlook. The Standard Ethics assessment reflects REVO’s strong commitment to sustainable value creation and accompanies the launch of the new three-year ESG plan addressing key policies such as Diversity & Inclusion, responsible artificial intelligence, procurement, and human rights. Preparatory activities have also begun for the voluntary drafting of the first Sustainability Report, scheduled for 2026 and referring to fiscal year 2025.

KEY PLAN AND ECONOMIC PERFORMANCE KPIs

Below are the main economic KPIs across the various reference time horizons.

The half-year figures confirm REVO’s ability to grow profitably, following a trajectory in line with the ambitions outlined in the Industrial Plan.

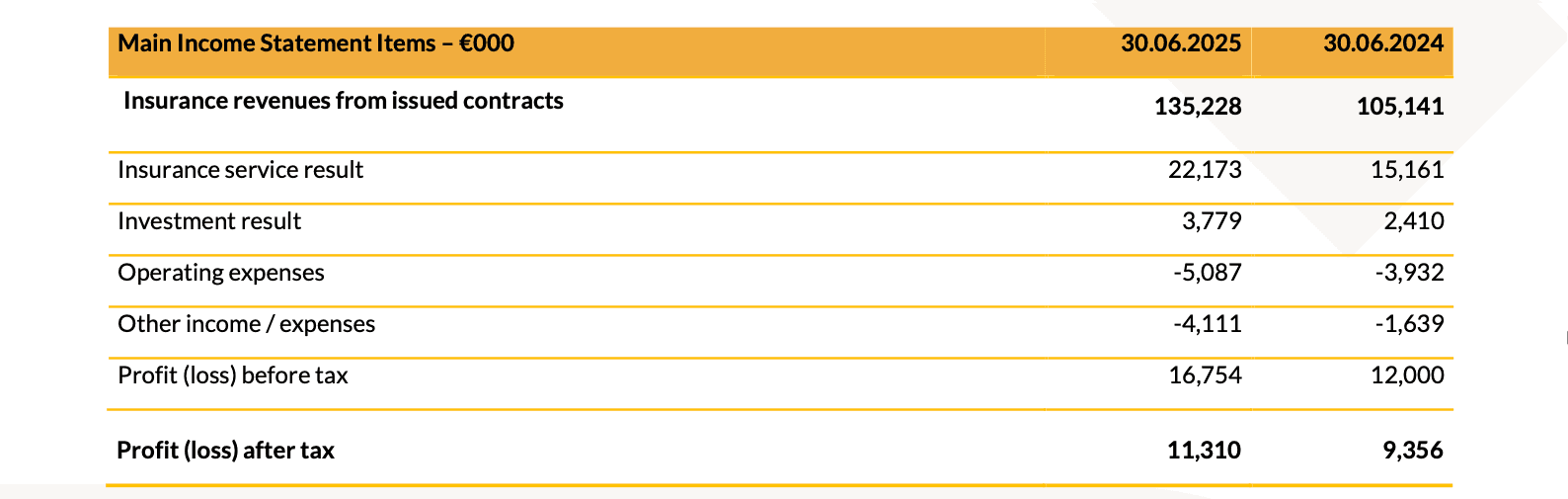

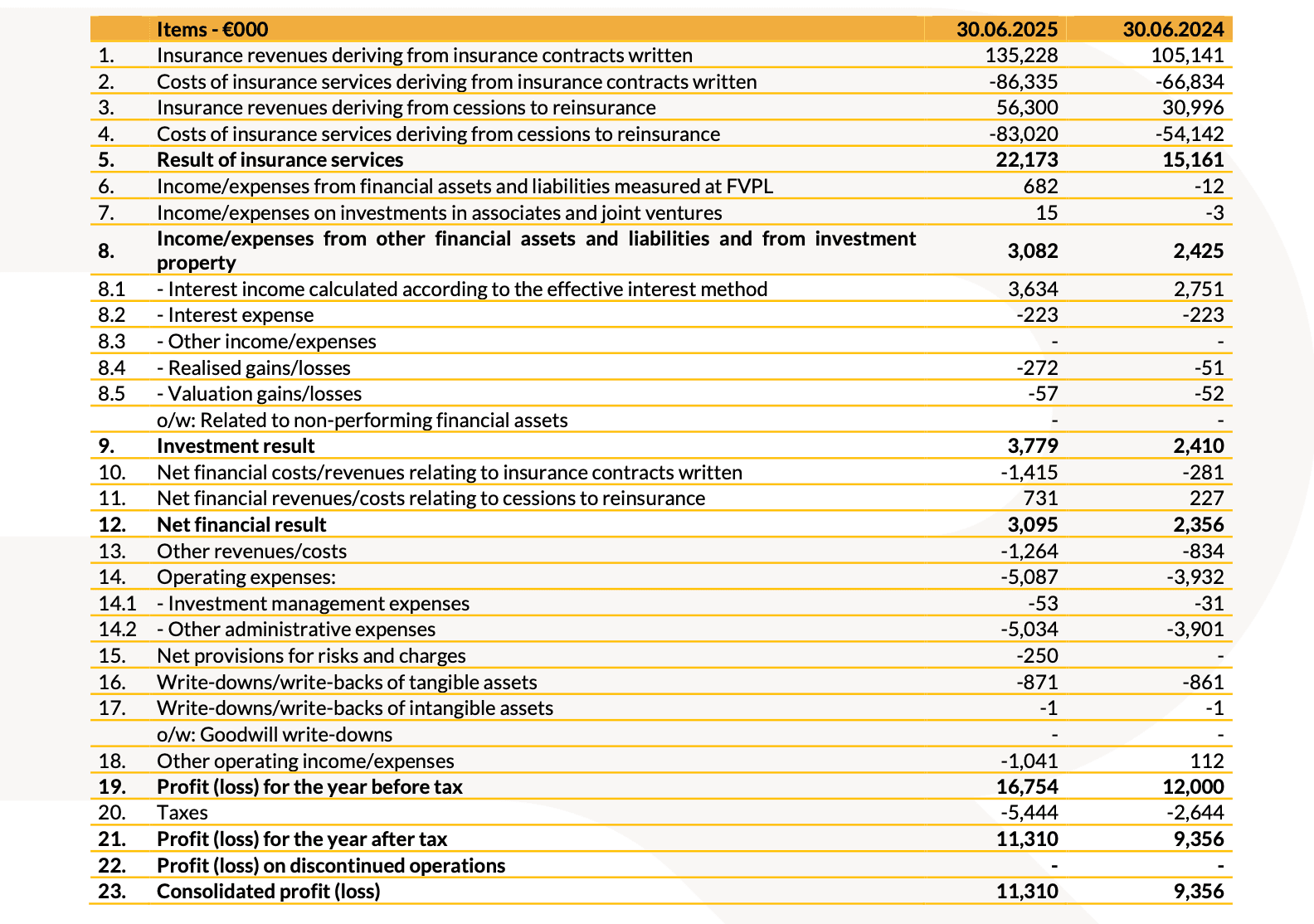

Below is a summary table highlighting the main items of the income statement recorded during the period:

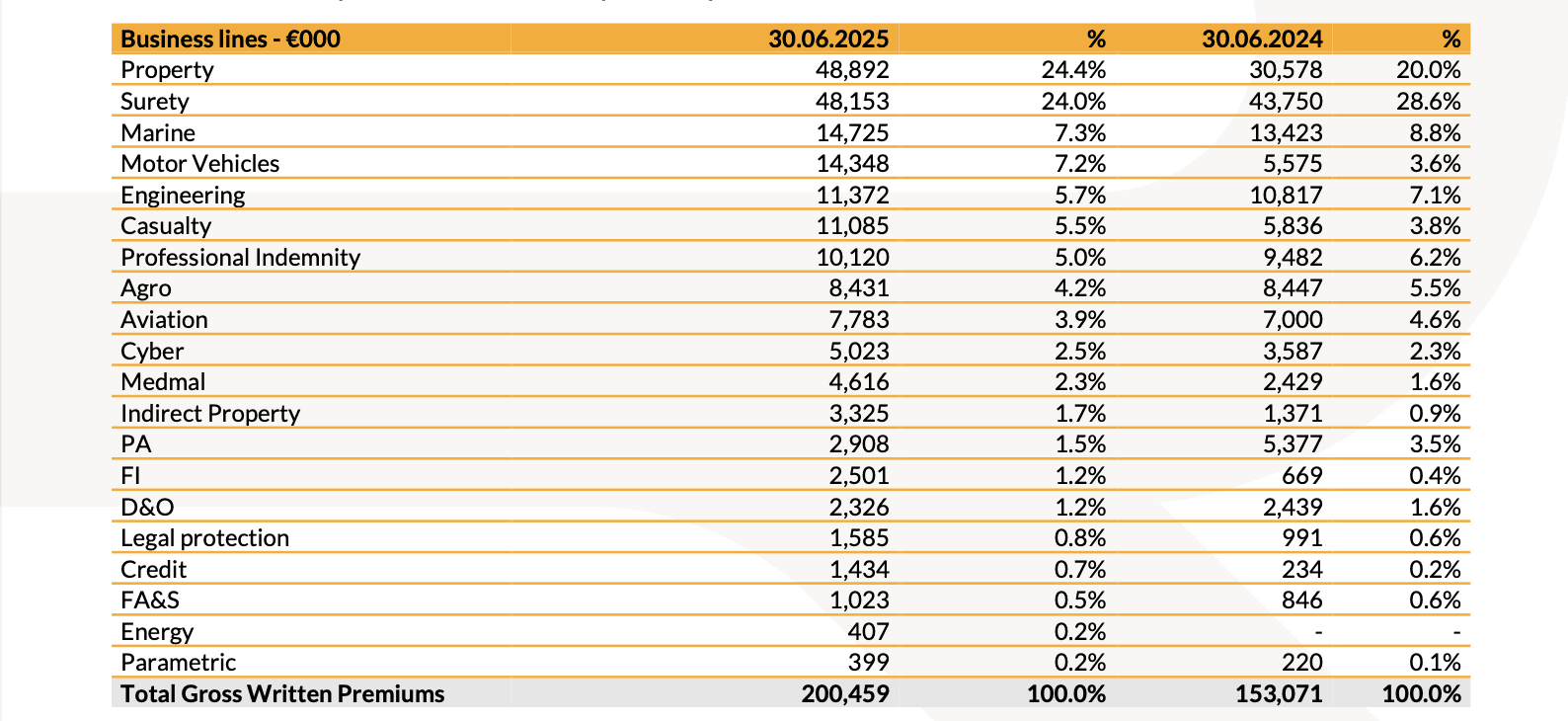

During the period, gross written premiums amounted to €200.5 million, with a significant increase compared to the same period in 2024 (+31.0%). Growth was recorded across all major business lines, with a particularly selective approach in certain segments (Agro, D&O, Personal Accident) aimed at preserving portfolio profitability.

As of 30th June 2024, the business mix was more diversified, with a tactical increase in exposure to the Property line, in response to particularly favorable underwriting conditions, and further expansion of the Surety business, which recorded a 10.1% increase during the half-year.

The table below provides a summary of the portfolio business mix as of 30 June 2025:

The Group’s operating performance in the first half of the year was driven by the following factors:

- Loss ratio increased compared to H1 2024 (32.3% vs. 29.4%), particularly in the MAT and General Liability portfolios. Figures also reflect an additional and prudent strengthening of IBNR reserves for approximately €5.0 million compared to December 2024.

- Accrual-based acquisition ratio(5) stood at 18.1%, showing a slight increase compared to 16.9% in the same period of 2024, mainly due to the business mix underwritten during the period.

- Cost ratio(6) decreased (19.7%, down from 21.9% in H1 2024), due to lower insurance and general operating expenses—confirming improved operating leverage across the business.

- Personnel costs increased, driven by new hires and the temporary 2025-only MBO incentive plan (approximately €1 million).

- Reinsurance cost(7) incidence stood at 15.6%, down from 17.3% in the first half of 2024, thanks to higher ceded claims and increased commissions received from reinsurers compared to 2024.

- IT investments totaled approximately €5 million, also in connection with the new 2026–2028 Industrial Plan “THE TECHUMAN ERA.”

- As a result of these dynamics, the gross Combined Operating Ratio(8) (COR) for the period stood at 83.2%, an improvement from 84.9% in H1 2024 and 85.8% at the end of fiscal year 2024. Lastly, a positive contribution from the investment portfolio is reported, with a result of €3.8 million, compared to €2.4 million in 2024. The new financial assets, which contributed to a further reduction in overall exposure to Italian risk, benefited from favorable market conditions, with low volatility resulting from their short duration.

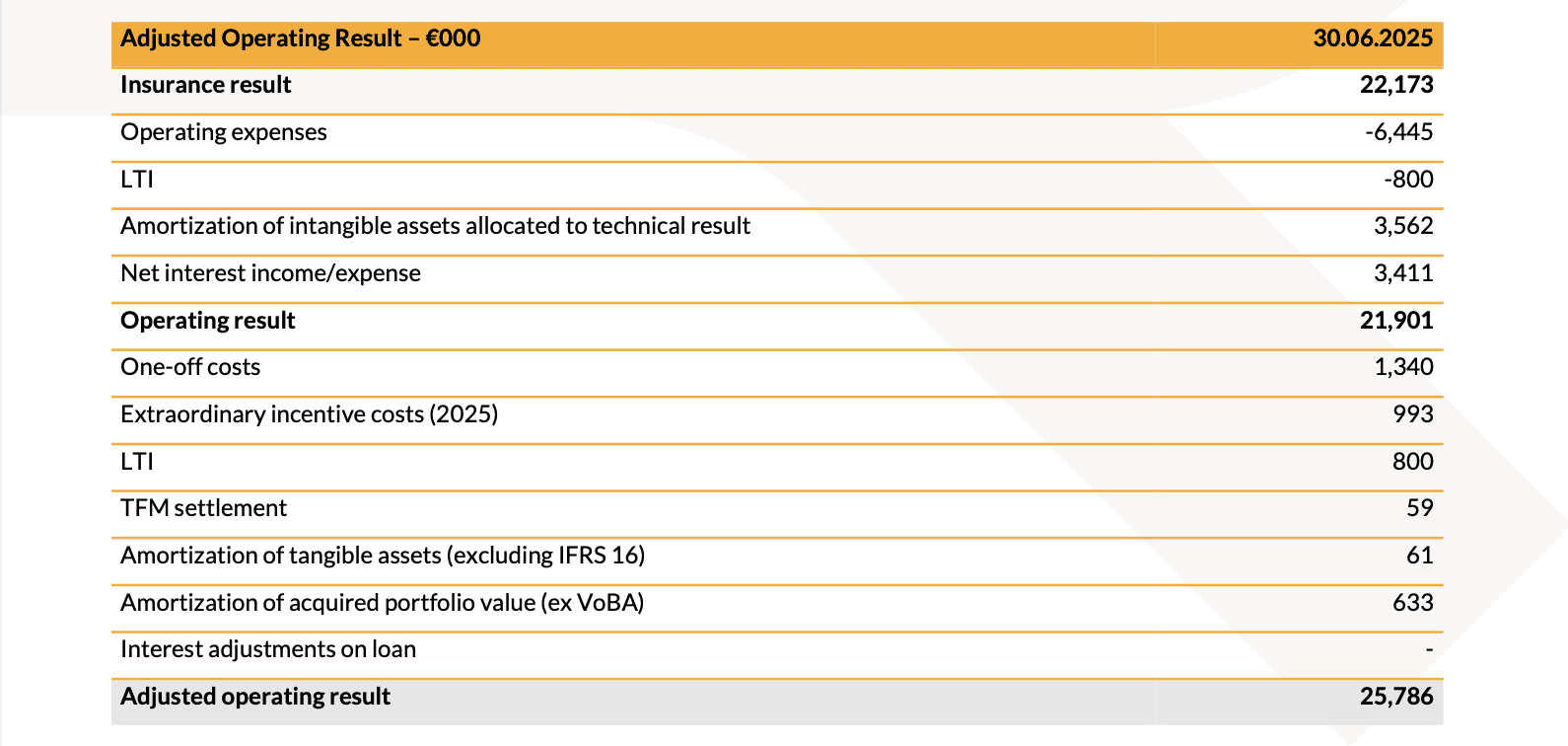

The following table provides the reconciliation of the adjusted operating result for the period:

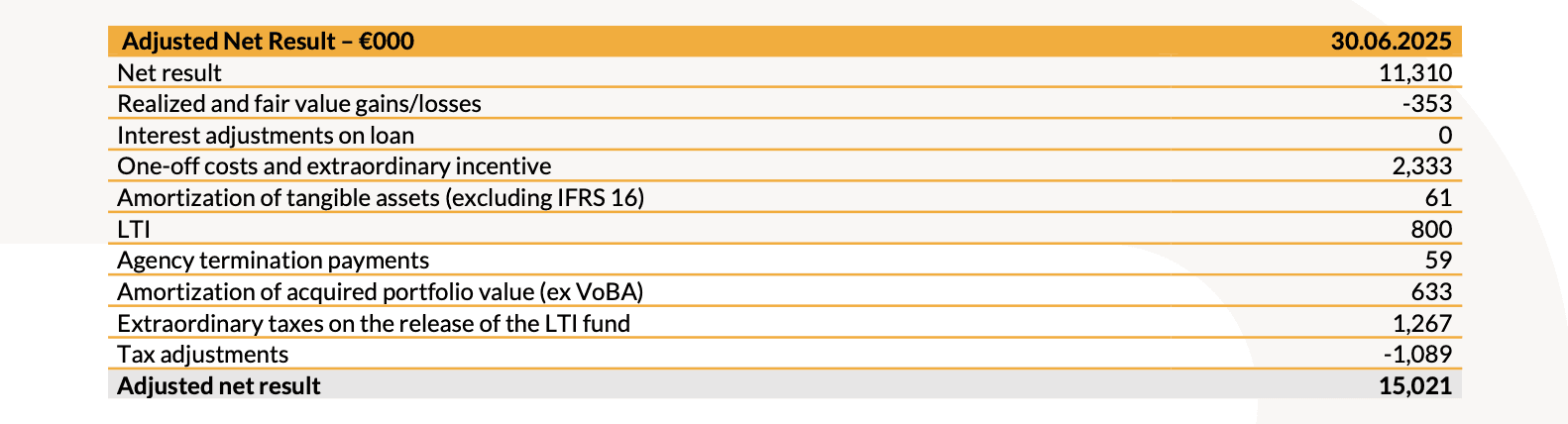

The following table provides the reconciliation of the adjusted net result for the half-year period:

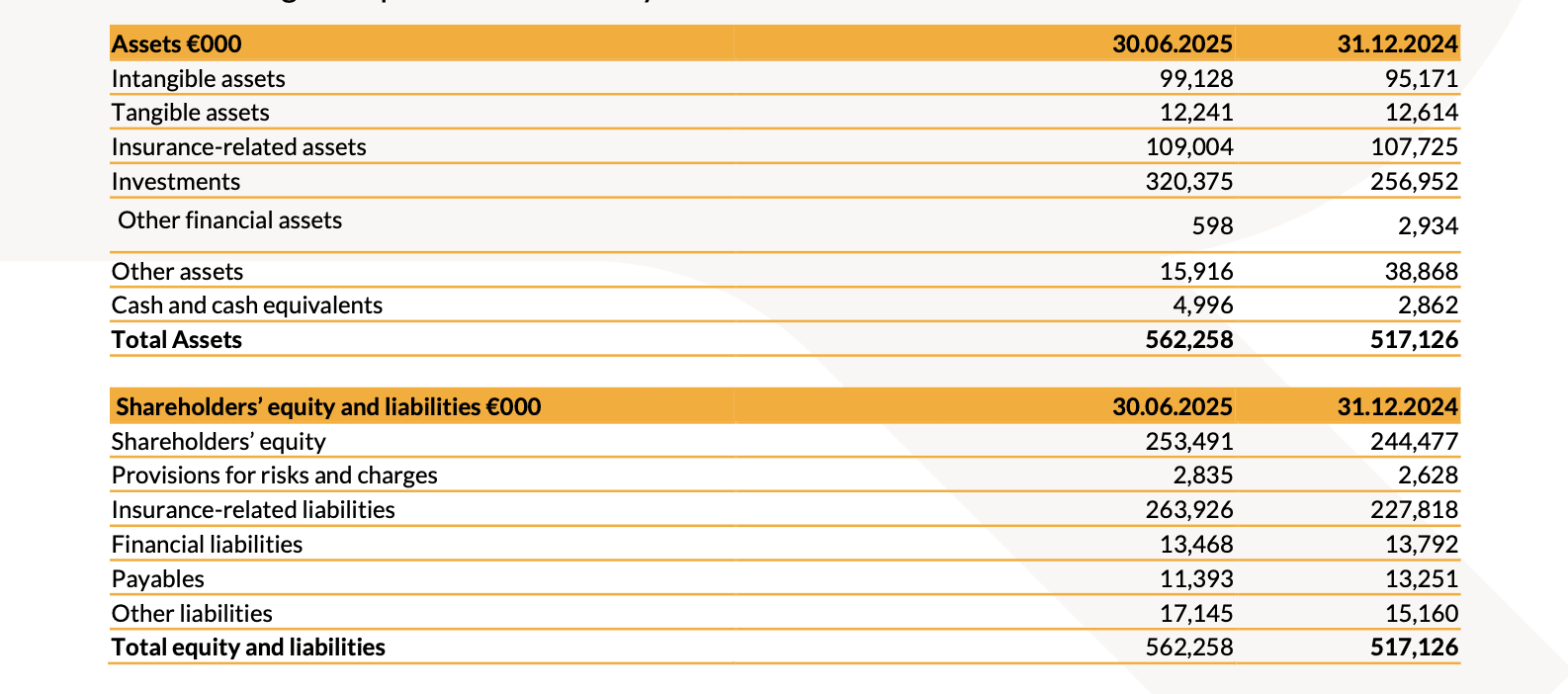

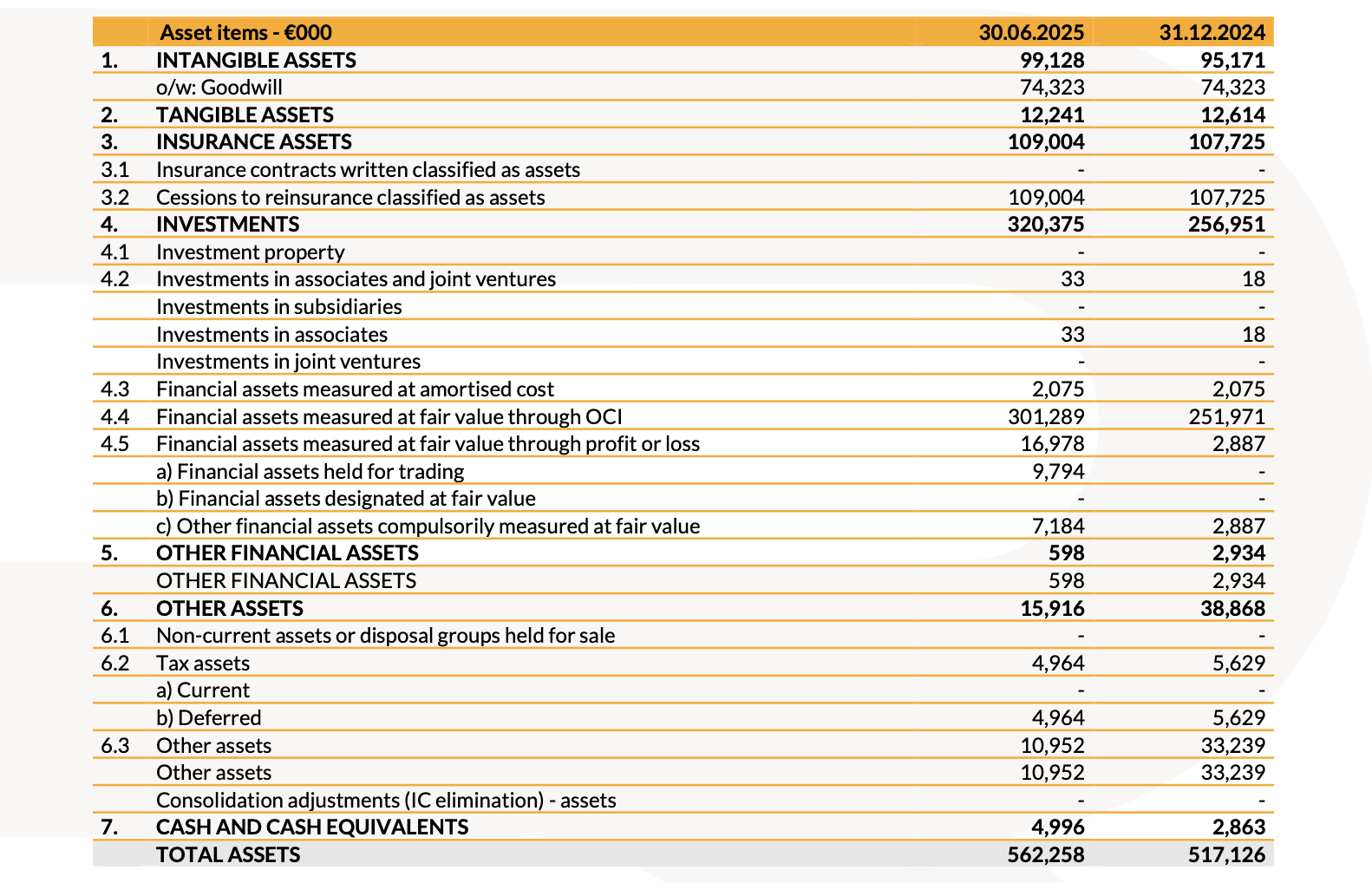

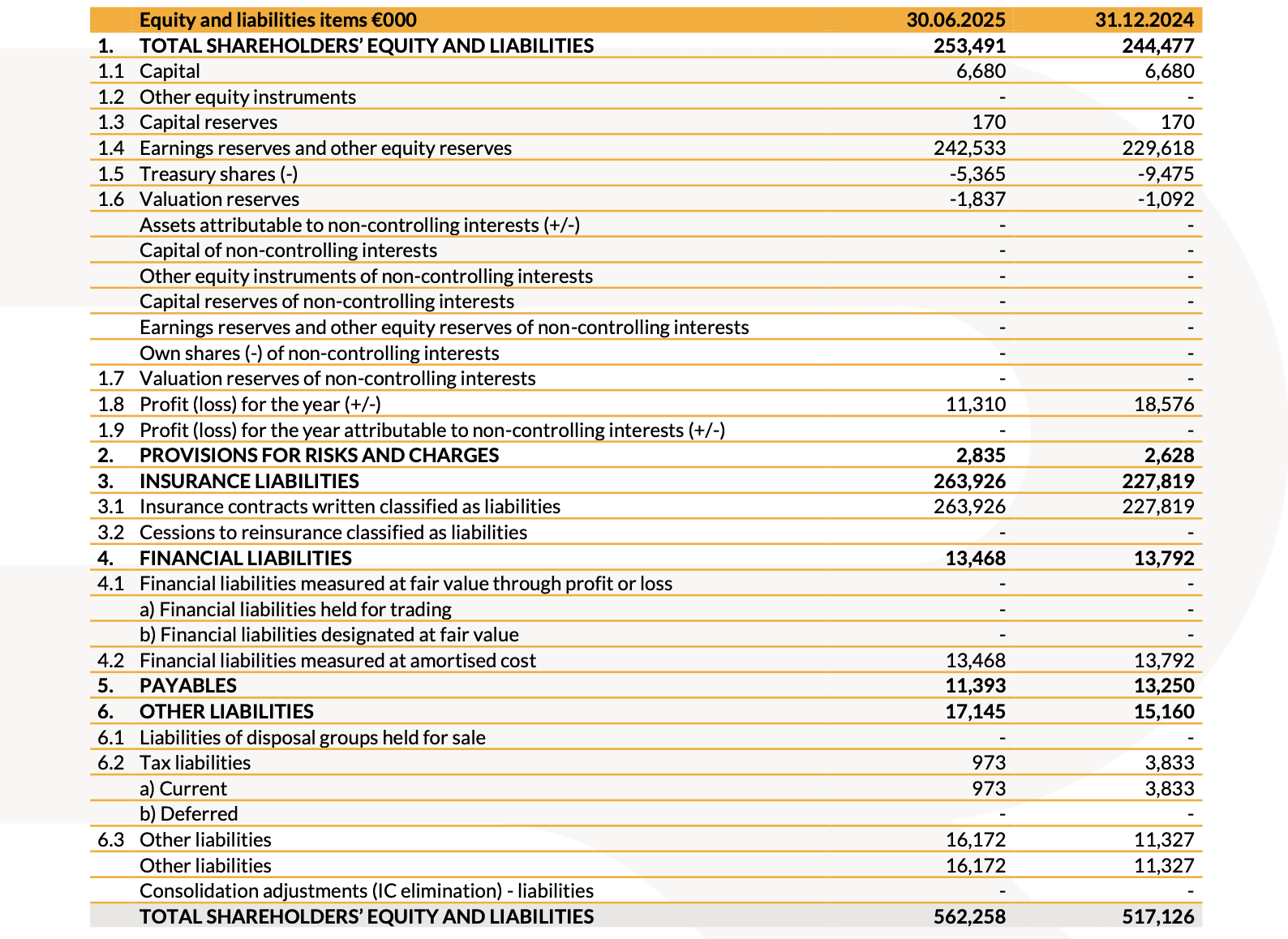

STATEMENT OF FINANCIAL POSITION

The following table presents a summary of the balance sheet:

Shareholders’ equity at the end of the period amounted to €253.5 million, an increase compared to €244.5 million as of 31st December 2024. Following the allocation of treasury shares to beneficiaries of the 2022–2024 LTI stock-based incentive plan, carried out in June 2025, the Company currently holds a total of 569,155 treasury shares, representing approximately 2.162% of the share capital, consisting solely of ordinary shares.

Confirming the Group’s strong capital position, the Solvency II Ratio as of 30th June 2025, stood at 245.2%, in line with the figure recorded as of 31st March 2025, which was 246.6%.

FINANCIAL REPORTING OFFICER

Pursuant to Article 154-bis of the Consolidated Law on Finance, the Manager responsible for preparing the company’s financial reports, Mr. Jacopo Tanaglia, declares that the accounting information contained in this press release corresponds to the documentary evidence, books, and accounting records.

The Company informs that the consolidated Half-Year Financial Report as of 30 June 2025 will be made available to the public at the registered office and on the website www.revoinsurance.com, in the manner and within the timeframe established by applicable laws and regulations.

The results as of 30 June 2025 will be presented to the financial community today at 6:00 PM (CET) via conference call. Dial-in numbers are: +39 02 802 09 11 (Italy), +44 1 212818004 (UK), and +1 718 7058796 (USA).

The presentation related to the results is available on the website www.revoinsurance.com in the Investor Relations section.

The consolidated balance sheet and income statement of REVO Insurance S.p.A. as of 30 June 2025 are attached below, with the note that the consolidated report and related documentation have not yet been certified by the independent auditors, nor have the Solvency II data, pursuant to IVASS Regulation no. 42 of 2 August 2018.

CONSOLIDATED INCOME STATEMENT

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

(1) Adjustments include recurring income and expenses from investments, and exclude one-off extraordinary costs (such as, for example, activities preparatory to the drafting of the 2026–2028 Industrial Plan and employee incentive plan costs, which are exceptionally planned only for fiscal year 2025, the amortisation of the acquired portfolio (former VoBA), and the cost of the LTIP), as well as other minor items, including the depreciation of tangible assets, severance payments (TFM), and financial debt-related costs

(2) IFRS 17 Combined Ratio = (Costs for issued insurance services + reinsurance result) / (Gross insurance revenue excl. VoBA)

(3) The calculation is based on the adoption of the Standard Formula and the use of Undertaking Specific Parameters (USP) for the Credit and Bonding lines.

(4) IFRS 17 Loss Ratio = (Gross incurred claims from direct and indirect business) / (Gross insurance revenue excluding commissions and VoBA)

(5) IFRS 17 Cost Ratio = (Total administrative expenses net of intangible asset amortisation + other operating income/expenses) / (Gross insurance revenue excluding commissions and VoBA)

(6) IFRS 17 Acquisition Ratio = (Total acquisition commissions) / (Gross insurance revenue excluding commissions and VoBA)

(7) IFRS 17 Reinsurance Cost Incidence = (Insurance revenues and expenses from reinsurance ceded) / (Gross insurance revenue excluding commissions and VoBA)

(8) Gross combined ratio IFRS 17 = (Costs for insurance services issued + reinsurance result) / (Insurance revenues before VoBA)