Verona, 3/16/2026

Consolidated Financial Results as at 31 December 2025

REVO CLOSES ITS TRANSITION YEAR BETWEEN TWO STRATEGIC PLANS WITH STRONG GROWTH AND IMPROVED OPERATIONAL EFFICIENCY DRIVEN BY TECHNOLOGICAL DEVELOPMENT

Gross written premiums close to € 400 million, with an adjusted operating result of € 48.4 million and a Solvency II ratio of 223.2%.

- Gross written premiums: € 398.1 million - Adjusted operating result: € 48.4 million

- Net profit: € 22.4 million

- Adjusted net profit: € 28.6 million

- Group Solvency II ratio: 223.2%

- Proposed dividend: € 0.27 per share

Verona, 16 March 2026 – The Board of Directors of REVO Insurance S.p.A., parent company of the REVO Insurance Group, approved today the consolidated results for the financial year ended 31 December 2025.

KEY INDICATORS

The 2025 financial year once again confirms strong growth across all economic and financial metrics, in line with the Group’s growth trajectory and fully consistent with its capital strength targets.

- Gross written premiums amounted to € 398.1 million, up +28.9% compared with the previous year (€ 308.8 million);

- Further profitable growth in the Surety line of business (27.1% of total premiums, with an increase of +13.5%), alongside greater exposure across all other lines of business (+35.8% compared with 2024);

- Strong technical profitability maintained, with an overall loss ratio[1] of 37.7% (37.3% as at 31 December 2024);

- Consolidated net profit reached € 22.4 million (up 20.6%), with adjusted net profit of € 28.6 million;

- Further development of the OverX platform, with € 15.3 million in investments aimed at strengthening and improving the efficiency of underwriting, claims management and distribution processes, through the adoption of new artificial intelligence solutions and enhanced data management systems;

- Positive contribution from the investment portfolio, exceeding annual targets, supported by a carefully management strategy focused on short duration and high diversification;

- Strong capital position confirmed, with a Group Solvency II ratio[2] of 223.2%;

- Proposed dividend of € 0.27 per share, up 22.7% compared with the dividend distributed on 2024 earnings (€ 0.22).

Alberto Minali, Chief Executive Officer of REVO Insurance, commented: “The results achieved confirm the strength of our operating model and represent the foundation for the execution of the ‘TECHUMAN ERA’ Strategic Plan. We continue to invest in proprietary technology, artificial intelligence and the development of our offer to support profitable growth and further enhance the quality of service provided to our distribution network. Exceeding € 100 million in premiums in the Surety line, the strong expansion of parametric solutions, and our international progress demonstrate REVO’s ability to combine innovation, specialization and scalability. On this basis, we will continue to strengthen our positioning in the specialty insurance market.”

STRATEGIC PERFORMANCE

During the financial year, the objectives set for the transition year between the two Strategic Plans were achieved. In particular:

- New developments for the proprietary OverX platform, with the addition of post-sales functionalities designed to ensure excellence in service to the distribution network, guaranteeing increasingly high standards of speed, control and quality;

- Further strengthening of Artificial Intelligence initiatives, in line with the “TECHUMAN ERA” Plan, confirming the central role of technology within the operating model. During the year, applications supporting the various business areas were further enhanced, resulting in greater efficiency, faster management processes and improved assessment quality. In particular, the Luminate assistant in the Underwriting area was further optimized, the self-assessment procedure in Surety was expanded and the Liquidate interface in the Claims area was strengthened. In parallel, preparatory activities were launched for the rollout of a targeted program aimed at enhancing digital skills, addressed to all employees;

- Strengthening of the product offering mix along the identified strategic directions. In addition to exceeding € 100 million in gross written premiums in the Surety business, consolidating leadership in the Italian market, the new multi-risk line “REVO per l’Impresa” was launched, starting with “REVO per la Microimpresa”. This solution is designed to simplify protection for SMEs and professionals, including catastrophic risks, through an instant quotation model on the proprietary platform;

- Confirmation of the growth trend in the parametric offering, expanded to the travel segment with the new “Volo Protetto” solution and further strengthening of the automated model. During the year, more than 100,000 policies were issued, more than doubling the volume of the previous year. 63% of claims were settled via Instant Payment, marking the transition from fast compensation to immediate compensation, with a further improvement in customer experience;

- Expansion of the distribution network, with 193 active intermediaries at year-end (123 agencies and 70 brokers). At the same time, in line with the strategy of strong territorial presence, the operational scope of REVO Underwriting was expanded, reaching around 350 active collaborations, and the bancassurance channel was launched through the agreement with Banco Desio for the distribution of the Cyber solution;

- Progress in the development path in the Iberian market, with the progressive strengthening of the organizational and commercial structure of REVO Iberia. The Branch exceeded € 9 million in gross written premiums, confirming the scalability of the operating model and the proprietary OverX platform. The governance model was also strengthened with the appointment of the new Branch Manager in early 2026, together with the consolidation of distribution relationships;

- Growth of the organizational structure, with 49 new hires compared with the previous year, mainly in the Underwriting, Operations and Data & Analytics areas. These hires are aimed at strengthening technical expertise and the overall efficiency of the operating structure;

- Confirmation of the “A-” rating by S&P and the “EE” (Strong) rating by Standard Ethics Rating in the area of sustainability, together with the maintenance of the UNI/PdR 125:2022 gender equality certification, confirming the structural integration of equity and inclusion principles within organizational processes and corporate governance.

KEY PLAN KPIs AND ECONOMIC PERFORMANCE

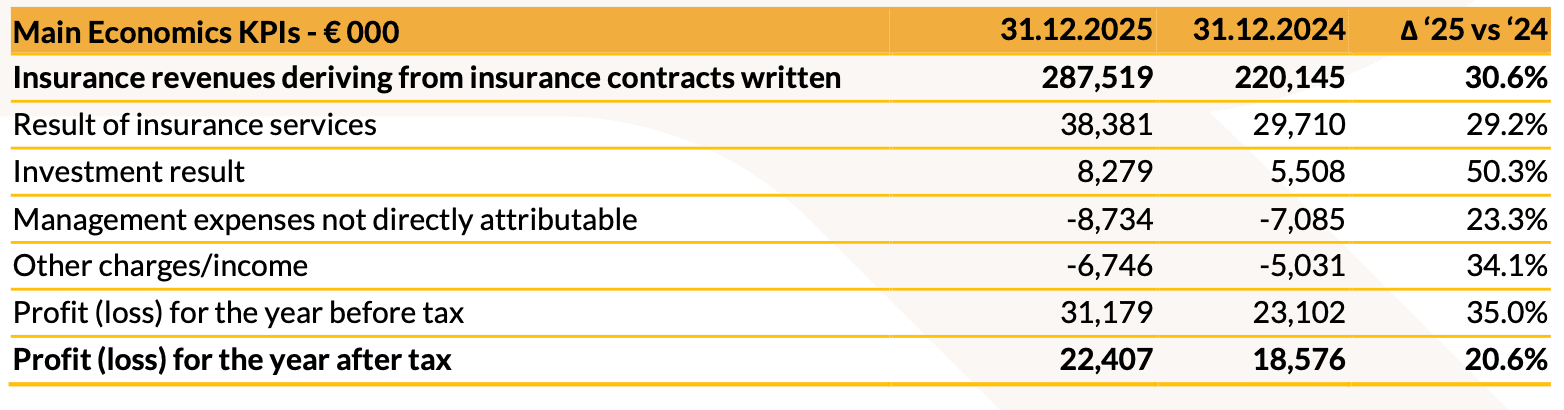

The table below shows the Group’s main economic KPIs recorded over the last three financial years:

The significant progress compared with the previous financial year is consistent with the growth trajectory outlined in the TECHUMAN ERA Plan, supported by the increase in premium growth and accompanied by a steady improvement in both operating and consolidated results, also confirmed in the latest financial year, which represents the transition year between REVO’s two Strategic Plans.

These figures demonstrate not only REVO’s ability to achieve consistent premium growth, but also the strength of its technical performance, which represents a key prerequisite for the orderly and profitable long-term development of the project.

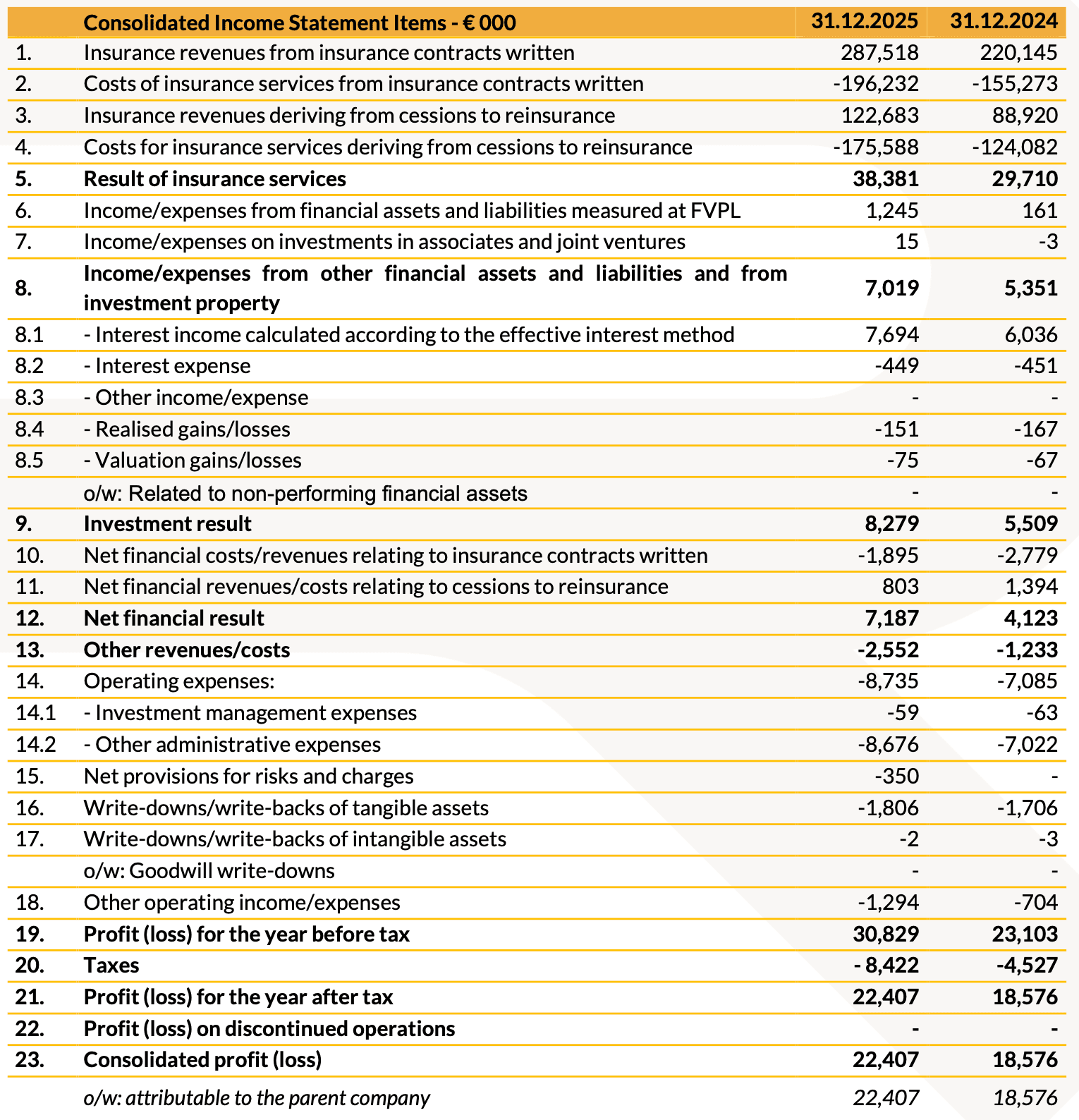

Below is a summary table highlighting the main income statement items recorded during the financial year.

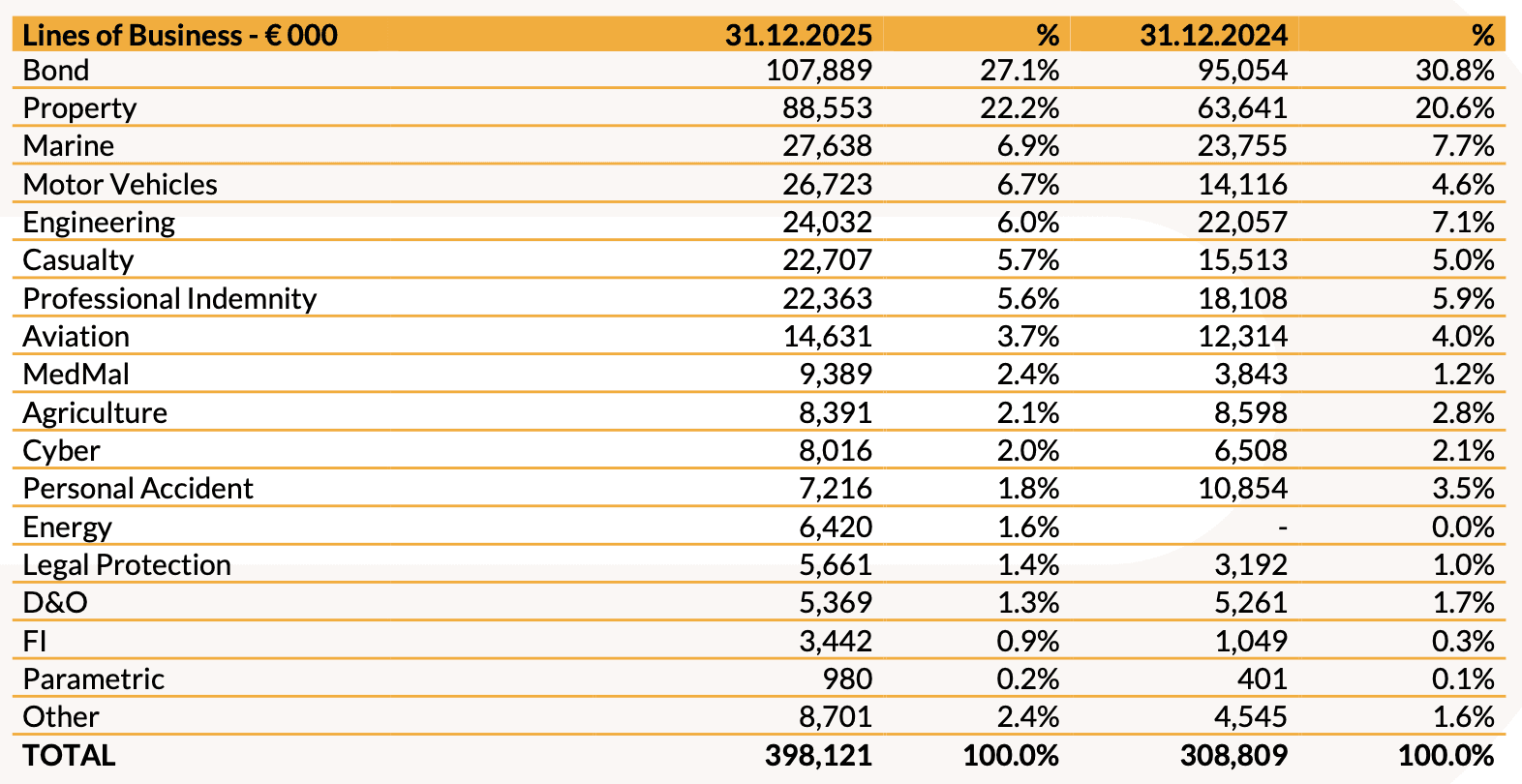

During the financial year, gross written premiums amounted to € 398.1 million, with a significant increase compared with 2024 (+28.9%). Growth was recorded across all lines of business, with the exception of Agriculture (where a particularly selective underwriting approach enabled the achievement of excellent technical performance, with a Loss Ratio of 39.5%) and Personal Accident (whose portfolio underwent a revision process, with the non-renewal of certain lower-profitability policies).

The Surety line of business recorded growth of 13.5% during the year, while confirming REVO’s leadership position in the Italian market in this segment, with gross written premiums of € 107.9 million.

As of 31 December 2025, the business mix became further diversified, fully consistent with REVO’s objective of becoming a leading player in the SME and professionals’ segment.

It is worth highlighting that during the year, thanks to the decisional agility that characterizes the initiative, REVO was able to grab significant opportunities in the Property segment, including through tactical approaches and particularly favourable technical conditions, thereby contributing to the strong growth of this line of business.

From an operational performance perspective, the economic results for the 2025 financial year were mainly driven by the following dynamics:

- Loss ratio in line with the medium-term development envisaged in the Plan, at 37.7% compared with 37.3% in 2024. In addition to the greater diversification of the business mix, it should be noted a further prudent strengthening of IBNR reserves of approximately € 6.8 million and provisions covering the expected ultimate cost (IBNeR) of approximately € 7.2 million. At the same time, REVO adopted statistical-actuarial models to further refine reserving calculations, improving the estimates underlying the reserve calculations.

- Acquisition ratio[3] of 17.0%, broadly in line with 17.1% recorded as of 31 December 2024;

- Cost ratio[4] further reduced (17.6% compared with 19.4% in 2024), reflecting a lower incidence of insurance costs and other operating expenses, confirming the ongoing improvement in the project’s operating leverage;

- Reinsurance[5] cost ratio of 14.7%, up from 12.6% in 2024, mainly due to a different business mix, the underwriting of certain large risks with higher reinsurance coverage, and a slight reduction in commissions received from reinsurers, partially offset by the higher share of ceded claims.

As a result of these dynamics, the gross combined ratio (COR)[6] for the period stood at 86.3%, slightly higher than 85.8% in 2024. This result remains consistent with the objective of reducing the COR to below 85% by 2028.

Finally, it is worth highlighting the positive contribution of the investment portfolio, with income of approximately € 8.3 million, compared with € 5.5 million in 2024. During the year, the portfolio was further diversified, with a reduction in overall exposure to Italian risk (30.5% compared with 34.1% as of 31 December 2024), alongside a greater contribution from non-Italian government securities (36.4% compared with 43.7%) and high-rating corporate bonds with short duration (27.8% compared with 20.1%).

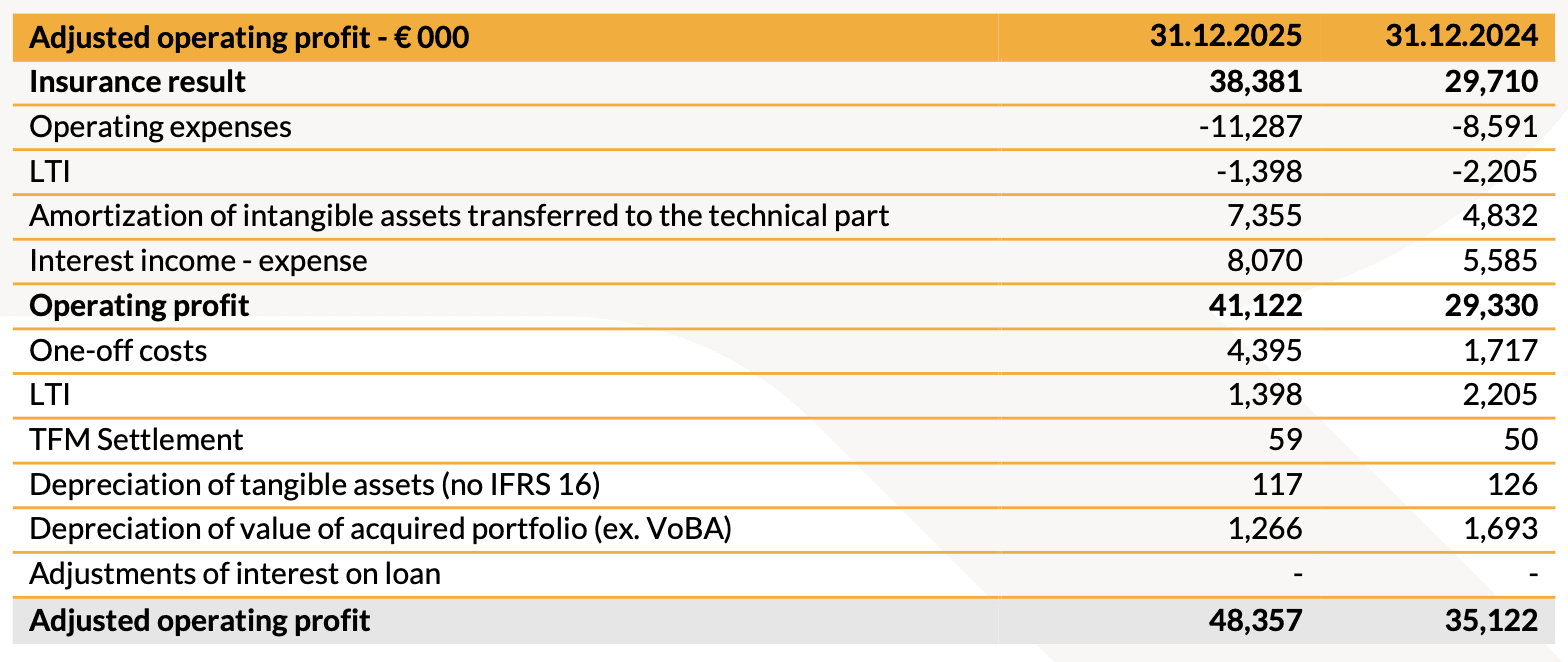

Below is the reconciliation statement relating to the Adjusted Operating Result for the financial year:

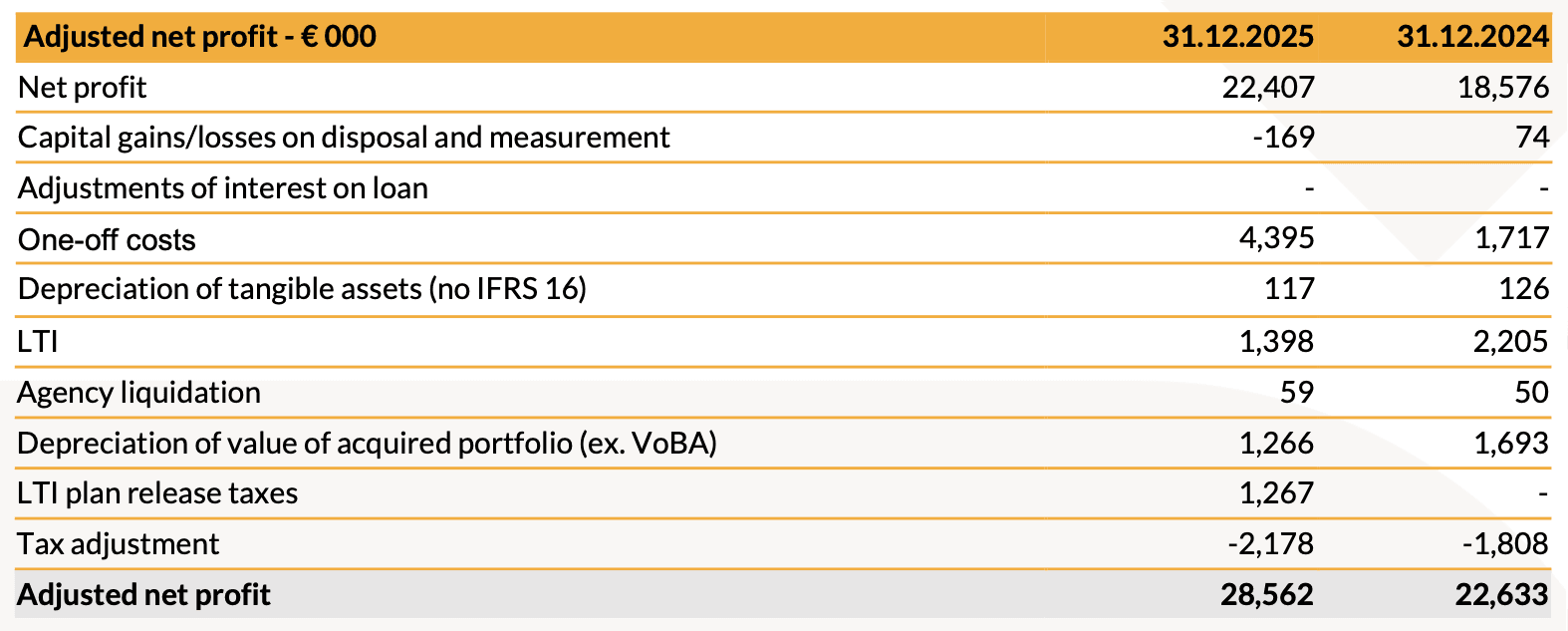

Below is the reconciliation statement relating to the adjusted net result for the financial year:

A higher tax incidence was recorded at the end of 2025 compared with the previous financial year.

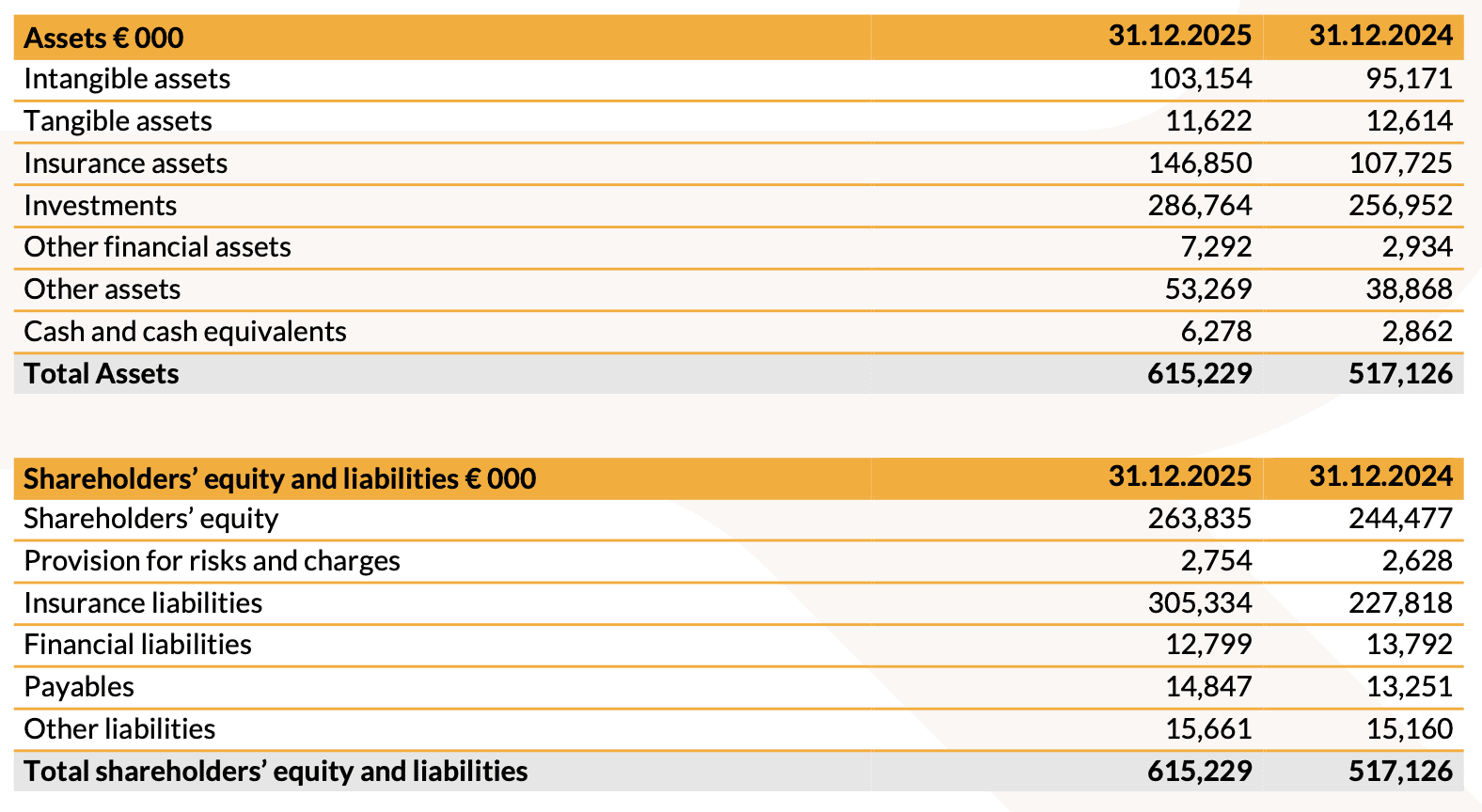

BALANCE SHEET POSITION

Below is a summary table of the Group’s balance sheet position:

Shareholders’ equity at the end of the financial year amounted to € 263.8 million, an increase compared with €244.5 million as of 31 December 2024. Following the allocation of treasury shares to beneficiaries of the LTI 2022–2024 incentive plan, as of 31 December 2025 REVO held 569,155 treasury shares, representing approximately 1.94% of the share capital[7].

The Group Solvency II ratio as of 31 December 2025 stood at 223.2%.

DIVIDEND

A dividend of € 0.27 per share will be proposed at the next Shareholders’ Meeting, corresponding to a dividend yield of 1.4% based on the closing price of REVO shares as of 31 December 2025.

The dividend will be payable starting from 6 May 2026. REVO shares will be traded ex-dividend from 4 May 2026, with the record date set for 5 May 2026.

MANAGER IN CHARGE OF FINANCIAL REPORTING

The Manager in charge of preparing the company’s financial reports, Dr. Jacopo Tanaglia, declares, pursuant to Article 154-bis of the Consolidated Law on Finance, that the accounting data contained in this press release corresponds to the company’s accounting records, books and supporting documentation.

The Company informs that the Separate Financial Statements and the Consolidated Financial Statements as of 31 December 2025 will be made available to the public at the Company’s registered office and on the website www.revoinsurance.com, in accordance with the procedures and within the timeframes required by applicable laws and regulations.

The results as of 31 December 2025 will be presented to the financial community today at 18:00 (CET) via conference call. The dial-in numbers are: +39 02 802 09 11 (Italy), +44 1 212818004 (UK) and +1 718 7058796 (USA).

The presentation relating to the results is available on www.revoinsurance.comin the Investor Relations section.

Attached below are the reclassified consolidated and summary statements of financial position and income statement of REVO Insurance S.p.A. as of 31 December 2025. Please note that the separate and consolidated financial statements and the related documentation have not yet been audited by the external auditing firm, as well as the Solvency II data, pursuant to IVASS Regulation No. 42 of 2 August 2018.

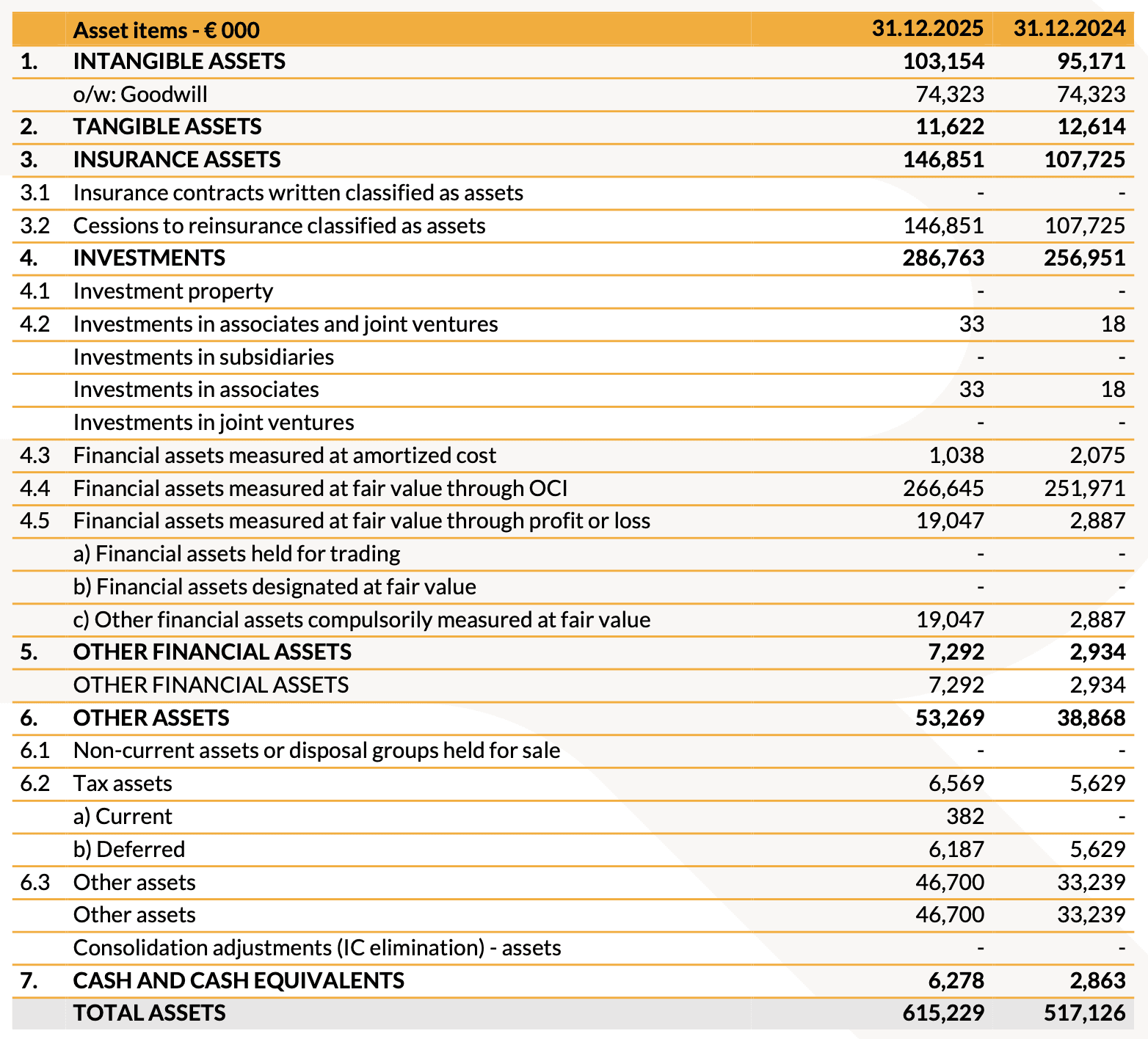

CONSOLIDATED STATEMENT OF FINANCIAL POSITION – ASSETS

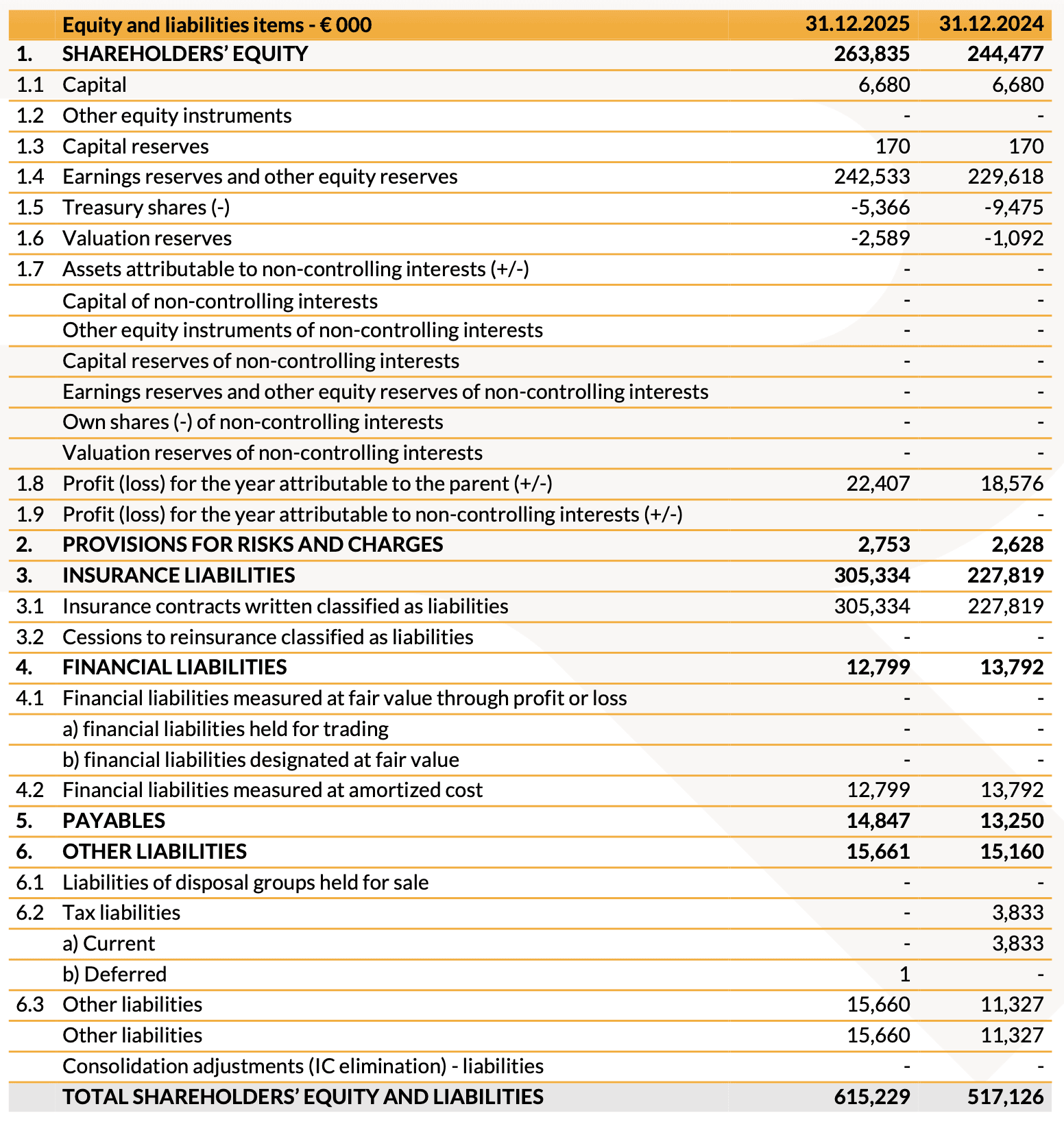

CONSOLIDATED STATEMENT OF FINANCIAL POSITION – EQUITY AND LIABILITIES

CONSOLIDATED INCOME STATEMENT

[1] IFRS 17 Loss Ratio = (Gross claims incurred from direct and indirect business) / (Insurance revenue before commissions and VoBA)

[2] On 5 February 2025, REVO Insurance obtained authorization from IVASS, pursuant to Article 45-sexies, paragraph 7, of the Italian Insurance Code, to use Undertaking Specific Parameters (USP) and Group Specific Parameters (GSP) for the Credit and Surety lines of business.

[3] IFRS 17 Acquisition Ratio = (Total acquisition commissions) / (Insurance revenue before commissions and VoBA).

[4] IFRS 17 Cost Ratio = (Total operating expenses net of amortisation of intangible assets + other operating expenses/income) / (Insurance revenue before commissions and VoBA).

[5] IFRS 17 Reinsurance Cost Ratio = (Insurance revenues and expenses arising from reinsurance cessions) / (Insurance revenue before commissions and VoBA).

[6] IFRS 17 Gross Combined Ratio = (Insurance service expenses incurred + reinsurance result) / (Insurance revenue before VoBA).

[7] Share capital consisting exclusively of ordinary shares as of 31 December 2025.