Milano, 5/14/2026

Consolidated Results as at 31 March 2026

REVO: A SOLID TECHNICAL PERFORMANCE AT THE START OF THE YEAR, WITH IMPROVING KEY INDICATORS

Gross written premiums to € 115.8 million (+13.0% compared to the first quarter of 2025), also driven by the growth of REVO Iberia, with adjusted operating result¹ to € 13.6 million and adjusted net profit to € 8.2 million.

Consolidated Results:

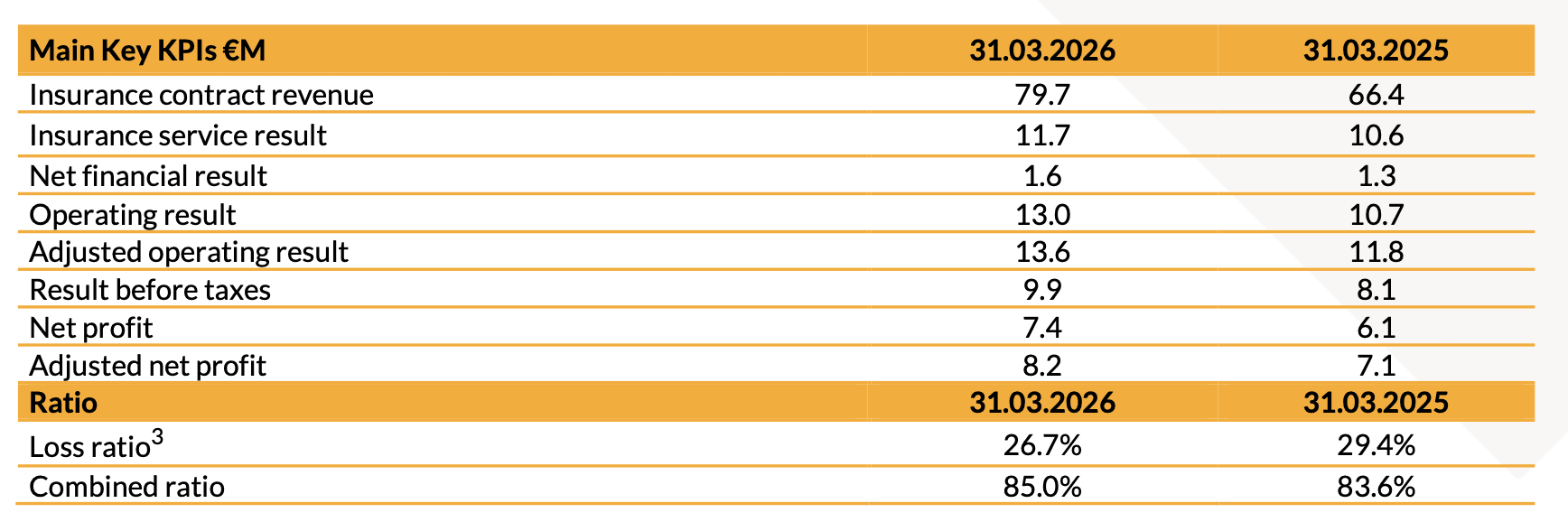

Insurance contract revenue: € 79.7 million

Insurance service result: € 11.7 million

Net financial result: € 1.6 million

Operating result: € 13.0 million

Adjusted¹ operating result: € 13.6 million

Net profit: € 7.4 million

Adjusted net profit¹: € 8.2 million

Combined ratio²: 85.0%

Group Solvency II ratio: 224.1%

Milan, 14 May 2026 - The Board of Directors of REVO Insurance S.p.A., the parent company of the REVO Insurance Group, approved today the consolidated results for the first quarter of 2026.

STRATEGIC PERFORMANCE DURING THE QUARTER

During the quarter, the following activities are highlighted:

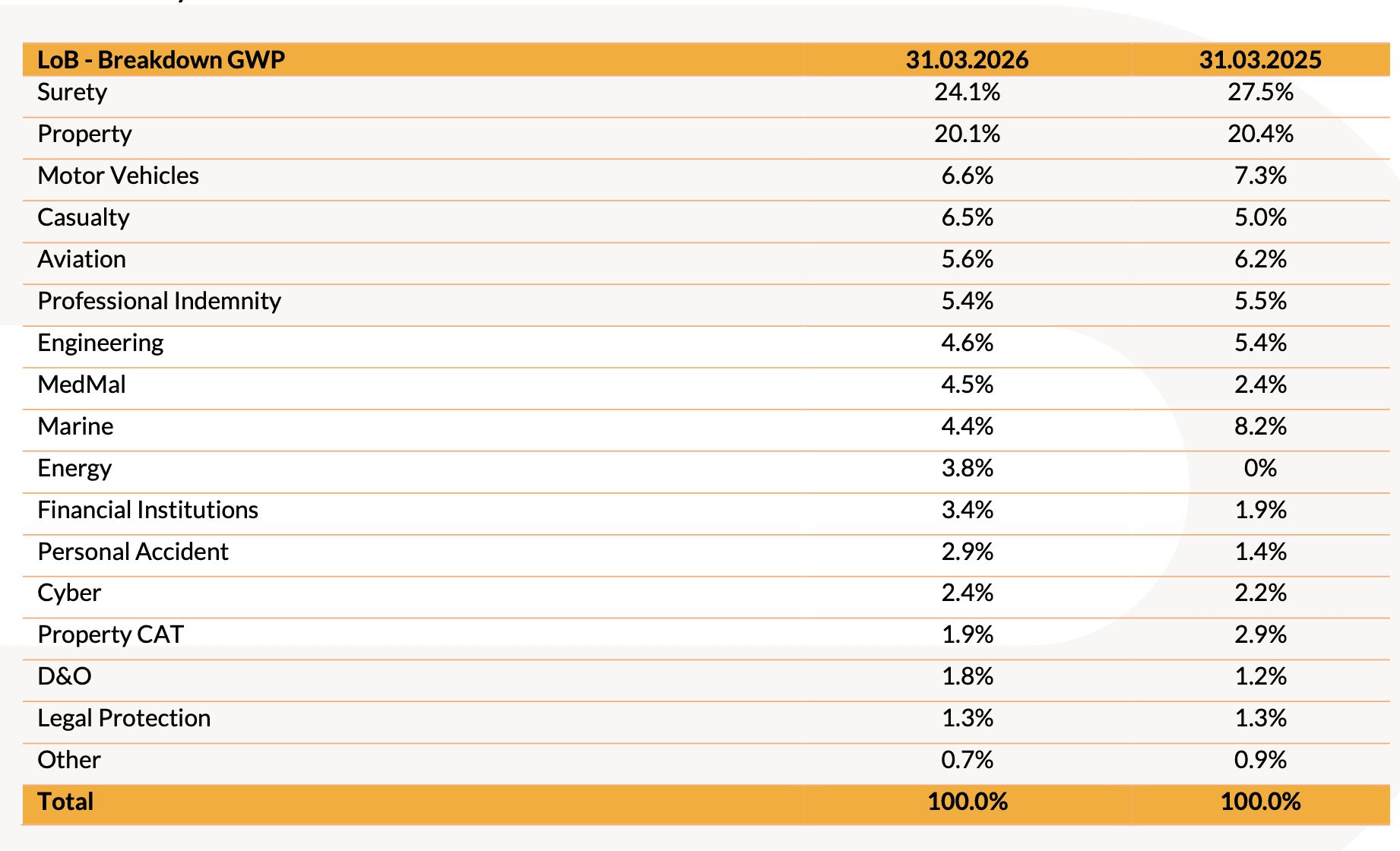

A high level of diversification of the overall insurance portfolio was maintained, as shown in the summary table below:

Progress in the development path in the Iberian market, through the gradual consolidation of agreements with local and international brokers and the concurrent strengthening of REVO Iberia’s operating and commercial structure (+2 new hires), in support of growth objectives. The Spanish branch closed the quarter with gross written premiums of € 4.5 million (up 91.7% compared to the same period in 2025);

Within the development path of the Specialty offering, new initiatives were launched, including:

the start-up of the Energy LoB, which recorded strong growth in the first quarter with gross written premiums exceeding € 4 million;

the introduction of the STARTLITE solution, as part of REVO per la Microimpresa, designed to address the needs of microenterprises seeking essential coverage against catastrophic events, leveraging proprietary technology developed for the product;

the integration of ESG criteria into the self-underwriting process of the Surety line of business, with incentive mechanisms providing for a 50% increase in the credit limit to clients with a positive ESG rating;

Growth in the parametric segment, supported by increasing demand for simple, immediate and highly innovative coverage solutions. In the first quarter of 2026, policies issued reached 15,500 (+93% compared to the same period in 2025), mainly driven by the strong performance of REVO Protezione Consumi;

Consolidation of the distribution network, with 209 active intermediaries (124 agencies and 85 brokers). At the same time, confirming the strategy of strong territorial presence, the operating scope of REVO Underwriting was expanded, with approximately 360 active partnerships;

In line with the strategy of developing innovative and complementary distribution channels, starting from the end of March a partnership was launched with Satispay for the commercialization of an embedded group policy covering catastrophic risks, with a parametric component. The policy, integrated into the ‘Business Premium’ service, is automatically distributed to a network of over 450,000 merchants;

Further strengthening of Artificial Intelligence applications as part of the ongoing evolution of the OverX platform, in line with the guidelines of the Industrial Plan ‘THE TECHUMAN ERA’, with a focus on operational efficiency and scalability, while maintaining human oversight in decision-making processes. In the underwriting area, innovation focused in particular on D&O products, with the introduction of AI-based solutions enabling faster quotation processes and improved quality of risk assessments. In the claims area, the scope of automation was expanded across the opening and management phases, including under exclusive delegation, delivering benefits in terms of reduced manual activities, enhanced service timeliness (24/7) and overall process efficiency;

The addition of 19 new hires, primarily in the Underwriting and Operations areas, with a particular focus on Data & Analytics and Underwriting profiles, in line with the evolution of ‘THE TECHUMAN ERA’ Plan and aimed at strengthening underwriting capabilities and enhancing technological expertise;

Implementation of initiatives supporting the consolidation of the Group’s first Sustainability Report.

KEY PERFORMANCE INDICATORS – Q1 2026

The table below provides a summary of the Group’s principal KPIs as at 31 March 2026:

In particular, the following items were noted during the period:

Against gross written premiums of € 115.8 million, insurance contract revenue amounted to € 79.7 million, up 20.0% compared to the same period in 2025;

Confirmation of a high level of overall technical profitability, with a gross loss ratio of 26.7%, improving compared to the first quarter of 2025 (29.4%), reflecting the strong discipline that has consistently characterized the Group’s underwriting activity;

Insurance service result, net of costs directly attributable to insurance contracts and reinsurance dynamics, amounted to € 11.7 million (€ 10.6 million as at 31 March 2025). The cost ratio decreased (19.6% vs. 23.5% in the same period of 2025), driven by the progressive improvement in operating leverage, supported by the increasingly widespread adoption of AI solutions to assist people activities;

The acquisition ratio of the intermediated business during the period stood at 17.2%, improving compared to 18.5% in the first quarter of 2025, confirming the progressive optimisation observed over recent quarters;

During the period, the incidence of reinsurance⁴ costs increased to 20.6%, compared to 13.4% in the first quarter of 2025. The increase is attributable for approximately 5.4 percentage points to lower claims ceded, in a context of strong gross technical performance for the quarter, and for approximately 1.1 percentage points to a reduction in commissions, consistent with the gradual reallocation across certain lines of business towards non-proportional treaties;

As a result of these technical, operational and reinsurance dynamics, the combined ratio stood at 85.0%, higher than the same period of 2025 (83.6%), but improving compared to the level recorded at the end of the 2025 financial year (86.3%);

Net financial result amounted to € 1.6 million, of which the net contribution from investments was € 1.5 million. During the quarter, portfolio management continued along the diversification path, with a slight reduction in exposure to Italian sovereign risk to 29.8% (from 30.5% as at 31 December 2025) and an overall duration remaining at contained levels. The positive net inflows recorded during the period enabled the Group to seize attractive investment opportunities amid a volatile market environment;

Adjusted operating result amounted to € 13.6 million, up 15.2% compared to the first quarter of 2025, alongside an adjusted net profit of € 8.2 million, also increasing year on year. The comparison is influenced by higher adjustment components recorded in the first quarter of 2025 compared to 2026;

Group shareholders’ equity amounted to € 261.4 million.

SOLVENCY II

The Group’s capital position remains strong and above the medium-term targets set out in the Strategic Plan, with a Solvency II ratio⁵ at the end of the quarter standing at 224.1% (compared to 223.2% as at 31 December 2025). REVO therefore confirms its ability to autonomously generate the capital required to support its development.

TREASURY SHARES

As at 31 March 2026, the Company held a total of 569,155 treasury shares, representing approximately 1.94% of the share capital⁶, mainly allocated to support the employee incentive plan.

SECOND QUARTER OUTLOOK

In the current macroeconomic environment, characterized by uncertainty, REVO’s results have once again confirmed strong resilience from both an economic and capital perspective, with limited exposure to volatility arising from the political landscape and financial markets. REVO continues along its growth trajectory while maintaining a high level of technical quality, also in the first weeks of the second quarter of 2026.

EVENTS AFTER 31 MARCH 2026

It is hereby noted that the Shareholders’ Meeting, convened in both ordinary and extraordinary session on 27 April 2026, approved all the items on the agenda.

¹ IFRS 17 adjustments: including recurring investment income and expenses and commissions paid by REVO Underwriting to the distribution network; excluding depreciation of tangible assets, severance indemnity (TFM) settlements, extraordinary costs, financial debt costs, VoBA amortisation and LTIP.

² Gross IFRS 17 combined ratio = (Insurance service expenses incurred + reinsurance result) / (Gross insurance revenue before VoBA).

³ IFRS 17 loss ratio = (Gross incurred claims from direct and assumed business) / (Gross insurance revenue before reinsurance, commissions and VoBA).

⁴ IFRS 17 Reinsurance Cost Ratio = (Insurance revenues and expenses arising from reinsurance cessions) / (Insurance revenue before commissions and VoBA).

⁵ The calculation is based on the adoption of the Standard Formula, using Undertaking Specific Parameters (“USP”) and Group Specific Parameters (“GSP”) for the Credit and Surety lines of business.

⁶ Share capital, consisting exclusively of ordinary shares, amounting to 29,305,985.