Milano, 11/8/2023

REVO: High technical profitability confirmed with GWP target raised to over €200 million

As at 30 September 2023, premiums were up 84.6% compared to the first nine months of 2022, with an IFRS 17-adjusted operating profit1 of €19.5 million. The exit trajectory from the operational j-curve in the first half of 2023 is confirmed, with a further decrease of the cost rate. Thanks to the particularly positive trend in revenues, the Group increased its GWP target for the year from approximately €180 million to over €200 million.

In continuity with the positive performance recorded in financial year 2022 and in the first half of 2023, the results for the third quarter confirm the project’s potential and the strong attention that the market is reserving to REVO, thanks to its full range of insurance solutions and adoption of simple, fast operating processes for the benefit of intermediaries.

IFRS 17 results:

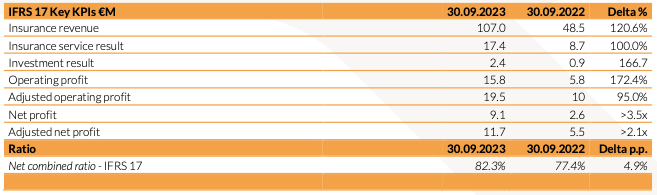

Insurance revenue €107.0 million

Insurance service result €17.4 million

Investment result €2.4 million

Adjusted¹ operating profit €19.5 million

Net profit €9.1 million

Adjusted¹ net profit €11.7 million

IFRS 17 combined ratio2 82.3%

IFRS 4 results:

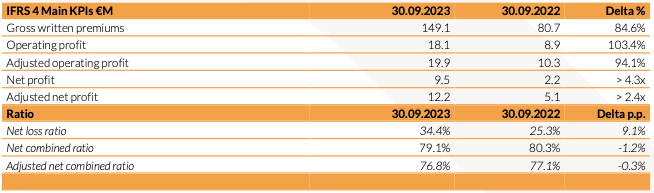

Gross written premiums €149.1 million

Adjusted¹ operating profit €19.9 million

Net profit €9.5 million

Adjusted¹ net profit of €12.2 million

Net loss ratio 34.4%

Net combined ratio² 79.1%

The Group's Solvency II ratio as at 30 September 2023 was 222.4% (234.7% at the end of the first half of 2023), higher than the medium-term target of the plan.

¹The adjustments include recurring investment income and expenses and exclude one-off extraordinary costs, depreciation of the acquired portfolio (ex-VoBA) and LTIP cost, as well as other items of small value, including depreciation of assets materials, TFM settlement and costs for financial debts.

²IFRS 17 CoR = (Costs of insurance service + reinsurance result) / (Gross insurance revenue + VoBA)

Milan, 9 November 2023 - The Board of Directors of REVO Insurance S.p.A., parent company of the REVO Insurance Group, approved the consolidated results for the third quarter of 2023.

STRATEGIC PERFORMANCE IN THE THIRD QUARTER

In the first nine months of 2023 the execution of the plan and the implementation of projects functional to the achievement of annual targets continued. As a result of the particularly positive trend in premiums, the Group increases its GWP target for the year from €180 million to over €200 million, with a positive impact on the cost rate, which continues to fall constantly, as well as from plan targets. In particular, the following activities should be noted:

Further expansion of the direct distribution network (+10 brokers and +2 agents compared to 31 December 2022), for a total of 63 brokers and 118 agencies as at 30 September 2023;

Signing of new delegate underwriting agreements by REVO Underwriting, Group MGA launched in 2022 with the aim of increasing the Company's distribution capacity;

Recruitment of new HC (+34 employees, including 4 managerial personnel) to further strengthen the workforce, which has been steadily growing since the first phases of the launch of the project;

Inauguration of the headquarters in Milan and opening of the new operating headquarters in Genoa, for more extensive development of the business:

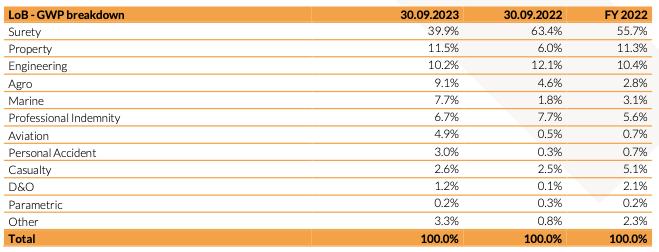

As per the 2022-2025 Business Plan, further diversification of the production mix. The table below summarises the breakdown of premiums by line of business:

Launch of new parametric products in the sectors Travel (REVO ParametricXFlight Delay and REVO ParametricXFlight Cancellation, parametric solutions for flight delay and cancellation, and REVO Specialty LiabilityX Travel Agencies, the third-party liability cover for travel agencies) and Agriculture (REVO ParametricXMosca Ulivo, the parametric solution based on IoT technology that covers damage caused by the olive fruit fly);

Expansion of OverX by including additional modules designed to simplify and automate processes, in both underwriting and claims management, with significant benefits for underwriters and intermediaries;

Further diversification of the investment portfolio, in a market context that remains favourable also considering the overall low duration of the managed portfolio.

MAIN IFRS 17 KPIs

In the scope of new international standard IFRS 17, considering the non-life business in which the company operates, and following the relevant eligibility tests provided for by the legislation, REVO adopts a simplified approach to quantifying the liability for remaining coverage (the "Premium Allocation Approach"), which as at 30 September 2023 did not differ materially from the IFRS 4 values.

The table below summarises the Group's main KPIs as at 30 September 2023 (presented in accordance with IFRS 17):

In particular, the following was reported during the period:

Gross written premiums of €149.1 million and revenues from insurance contracts (including

changes in the LFRC) of €107.0 million, with a significant increase on the same period of 2022;

Insurance service result of €17.4 million (compared with €8.7 million in the period ended 30 September 2022), net of costs directly attributable to insurance contracts and reinsurance dynamics;

The figures incorporate part of the catastrophic effects recorded during the third quarter, the final quantification of which is expected by the end of the year, with effects mitigated by the specific reinsurance cover in place;

IFRS 17 net combined ratio of 82.3%, up slightly compared with the same period of 2022 (77.4%) due to the different mix of the insurance portfolio and the different allocation under the new accounting standard of cost items attributable to insurance contracts;

Positive investment result of €2.4 million (income of €3.0 million), benefiting from the management activities implemented starting in the previous year;

Adjusted operating profit, pursuant to IFRS 17, of €19.5 million, with a positive effect - consistent with the expected plan trajectory - driven by a lower incidence of operating costs on generated business;

Consolidated net profit of €9.1 million;

Group shareholders’ equity of €220.1 million, up from the end-2022 value (€216.6 million).

MAIN IFRS 4 KPIs

The table below summarises the Group's main KPIs as at 30 September 2023 (presented in accordance with IFRS 4):

Specifically, the following was reported during the period:

Gross written premiums of €149.1 million, up 84.6% on the third quarter of 2022 (€80.7 million), thanks to growth recorded in all lines of business;

Further growth in the surety business line (+16.1% on the same period of 2022), mainly due to the significant expansion of the distribution network;

Maintenance of a good level of technical profitability despite the presence of several significant catastrophic events, with a total loss ratio³ of 34.4%, up from 25.3% in the third quarter of 2022, in line with the diversification of the portfolio underwritten;

Net combined ratio of 79.1%, up by approximately 1.2 percentage points compared to the same period of 2022 (85.5% as at 31 December 2022), driven by the same dynamics described above. This indicator on an adjusted basis was 76.8% during the period;

Positive investment contribution of approximately €2.4 million (income of €3.0 million), with a further diversification of the portfolio (exposure to Italian government risk of 41.9%), maintaining a low overall level of duration (approximately 2 years);

Consolidated net profit of €9.5 million, up significantly compared with the same period of 2022, and consolidated adjusted net profit of €12.2 million;

Group shareholders’ equity of €220.6 million, up from the end-2022 value (€216.6 million).

SOLVENCY II

Capital strength at Group level remains particularly high, with a Solvency II ratio⁴ of 222.4% at the end of the quarter (234.7% as at 30 June 2023). The nature variation is consistent with the forecast performance in the medium term and takes into account the strong growth of the business recorded in the period, as well as the voluntary partial takeover bid on REVO shares finalized during the first half of the year (Solvency II ratio value net of this operation equal to 231.2%).

OWN SHARES

As at 30 September 2023, 850,700 treasury shares are held in portfolio, equivalent to around 3.46% of share capital⁵.

FOURTH QUARTER OUTLOOK

The macroeconomic picture in the last few quarters has been dominated by the monetary policy decisions of the main Central Banks. The current context of geopolitical uncertainty will not affect REVO's ability to execute its business plan, which features funding objectives for the year that are higher than the initial targets. The Group will continue its programme of developing the main projects in progress, including the launch of new specialty and parametric products, the increasing use of the OverX platform, the expansion of the distribution network and the further strengthening of the management team.

³Loss ratio net of reinsurance

⁴CalculationbasedontheadoptionoftheStandardFormula

⁵Share capital comprising ordinary shares only

***

The Financial Reporting Officer, Jacopo Tanaglia, declares, pursuant to paragraph 2 of Article 154- bis of the Consolidated Law on Finance, that the accounting information contained in this press release matches those found in company documents, books and accounting records. The financial data contained in this press release has not been audited.